July 2017

By Ronald P. Bernardi

As of this writing, the State of Illinois began its fiscal year (July 1) without a budget for an unprecedented third year in a row. Sunday evening the Illinois House of Representatives approved a $36 billion spending plan that increases personal income taxes to 4.95% from the current 3.75% level and the corporate levy to 7% from 5.25%. If the Senate, which approved a tax hike last month, concurs on the House bill it will be presented to the governor for consideration. He has stated he will veto both the House and Senate spending bills as currently written.

Unfortunately, the Democrat controlled state legislature and Republican minority and governor have been unable to reach a compromise agreement. The opposing groups have failed to reach an agreement on how to balance revenues with expenditures, reduce growing pension costs and pay down the state’s backlog of overdue bills. As a result, the state’s credit rating is in jeopardy of falling into the “junk” status category. Such an event will likely further raise borrowing costs for most entities across the state.

Given these problems and the heightened uncertainty they create, we want to share some thoughts with you.

Clearly, the state’s financial situation is perilous and requires immediate remedy. The state is not yet Puerto Rico’s dystopian twin, but it is travelling in a dangerous direction. It remains uncertain to us whether opposing parties can come to some sort of agreement. Therefore, we remain wary of credits directly related to the state’s finances. As we have done for years, our portfolio managed accounts continue to avoid issues in this group.

Additionally, we remain wary of any sub-state credits OVERLY RELIANT on the state as a funding source. These municipalities are vulnerable to the vagaries and uncertainty of the state’s financial condition.

But NOT ALL issuers located in Illinois fall into the “overly reliant” category. Admittedly, it is a partially subjective determination defining “overly reliant” and we rely heavily on the analysis of our in-house municipal credit team to make these determinations. From these determinations we make certain investment decisions.

Making these determinations is the “art of municipal credit analysis” and an important reason our clients hire us to manage their bond portfolios.

We have heard and read some municipal market commentators state very broadly that municipalities in the State of Illinois are in trouble and that investors should avoid them or sell out of existing positions. These views are meaningless to us if there is no attendant detailed analysis of the specific issuer’s financial credit and its relationship with the state.

It seems to us there is a fair bit of “throwing the baby out with the bath water” occurring these days. And this creates opportunities, in our view.

So we suggest taking a deep breath. Please call us with your questions and justified concerns.

We will review the issuer’s credit standing, looking carefully at numerous credit metrics including:

- the sources of funding for the bonds

- the legal standing of the debt (UTGO, LTGO, COP, NOTE etc.)

- the purpose of the issuance

- its dependency on state funding

- its balance sheet and state of its general fund

After careful consideration of the Three Pillars of Credit Analysis, we can make an educated assessment as to an appropriate action.

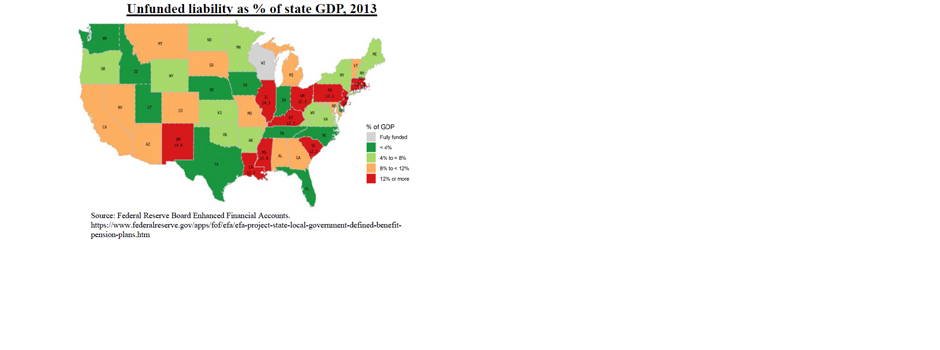

Undoubtedly, the continued inaction at the state level hurts investment and opportunities for businesses, residents and municipal governments across the state. Population and income growth in Illinois is stagnant and slightly negative when compared to most other parts of the country. Reducing taxpayers’ total liability (some measure at $300 billion) requires higher than average growth, so the stagnant economy since 2007 is clearly a negative metric. We expect the flat-lining or slow bleed of population will likely continue absent a political agreement to the state’s financial distress. But we do not conflate these negatives (and they are considerable) with widespread municipal defaults in Illinois.

Our approved list of Illinois-based credits and Illinois sector weighting has declined over the last 5-6 years while our surveillance efforts have greatly increased.

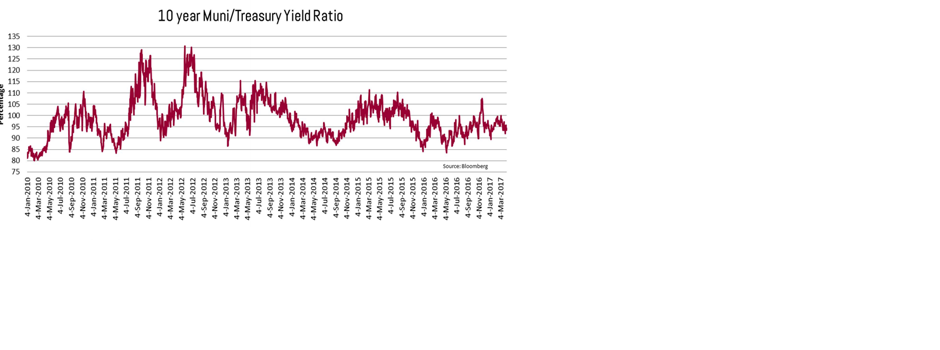

Yet the number of solid credits remains ample. Importantly, these issuers are forced to pay higher interest rates. The “Illinois Effect” offers value to knowledgeable investors and it is these values we seek.

Our in-house municipal credit department is one of our keys to uncovering these value opportunities. If you have questions or concerns about the credit quality of specific municipalities, please contact us and we can discuss completing a credit review.

If you are interested in learning about our municipal bond portfolio management platform we offer two options:

– fiduciary, fee only through our SEC registered investment advisory subsidiary, Bernardi Asset Management (BAM)

– non-fee, mark-up basis through parent company, Bernardi Securities, Inc. (BSI)

Please contact your Bernardi Investment Specialist for more information.

Thank you for your continued confidence and a happy Fourth of July holiday to all.

Sincerely,

Ronald P. Bernardi

President and CEO

July 3, 2017

Following Janet Yellen’s recent testimony, many investors may just want to wait for Federal Reserve policy makers to raise interest rates before committing money to the bond market. After all, the fed funds rate has been held in the 0% to 0.25% range for years so rates must go up, right? The answer is perhaps, but interest rate timers may have wasted four years waiting to catch a bigger fish – and just missed it. Most of the hike in

Following Janet Yellen’s recent testimony, many investors may just want to wait for Federal Reserve policy makers to raise interest rates before committing money to the bond market. After all, the fed funds rate has been held in the 0% to 0.25% range for years so rates must go up, right? The answer is perhaps, but interest rate timers may have wasted four years waiting to catch a bigger fish – and just missed it. Most of the hike in

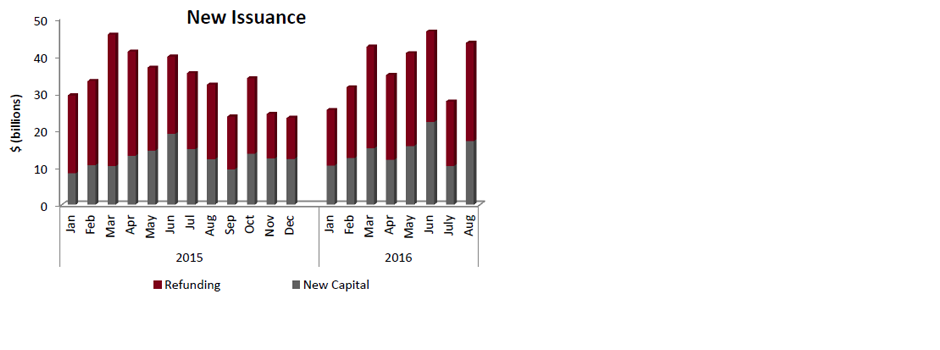

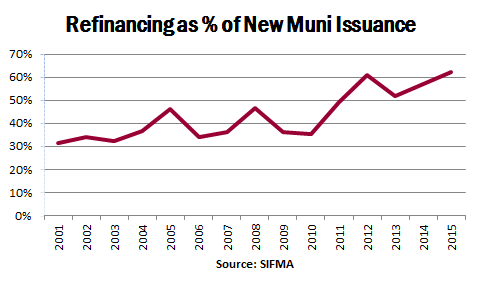

The total dollar value of the municipal market has barely grown since the 2008-2009 crisis. Outstanding debt totaled $3.77 trillion at the end of 2015, up from $3.54 trillion in 2006 (1). Corporate issuers have much more aggressively taken advantage of low rates. In fact, they have added an amount of debt almost equal to the size of the municipal market. Outstanding corporate debt has grown from $4.84 trillion in 2006 to $8.1 trillion at the end of 2015. It remains to be seen if this increased corporate leverage will lead to investment and future growth.

The total dollar value of the municipal market has barely grown since the 2008-2009 crisis. Outstanding debt totaled $3.77 trillion at the end of 2015, up from $3.54 trillion in 2006 (1). Corporate issuers have much more aggressively taken advantage of low rates. In fact, they have added an amount of debt almost equal to the size of the municipal market. Outstanding corporate debt has grown from $4.84 trillion in 2006 to $8.1 trillion at the end of 2015. It remains to be seen if this increased corporate leverage will lead to investment and future growth.  These dynamics are undeniably good news for the underlying credit health of municipal issuers. They are a prudent reaction in a paltry growth environment. Long term, however, municipalities face mounting pressure from defined benefit pension liabilities. At the end of June 2015 Wilshire Consulting reported that U.S. city and county pensions had 70 percent of the assets needed to meet their obligations to retirees.

These dynamics are undeniably good news for the underlying credit health of municipal issuers. They are a prudent reaction in a paltry growth environment. Long term, however, municipalities face mounting pressure from defined benefit pension liabilities. At the end of June 2015 Wilshire Consulting reported that U.S. city and county pensions had 70 percent of the assets needed to meet their obligations to retirees.