Why Warren’s Advice May Be Wrong for You

March 2, 2018

By Matthew P. Bernardi

Warren Buffett’s annual letter is one of the best insights into the mind of perhaps the greatest stock picker in history. His letters offer a great window into how he built a $500 billion conglomerate of businesses from a mere, mid-size textile manufacturing company. Today, Berkshire Hathaway intersects with our lives in myriad ways from auto insurance to underpants to home brokerage services. The man, however, is not without his biases as it pertains to financial markets and asset allocation, including a distaste for active stock management, investment bankers, and bonds.

The latter is the focus of this commentary and why individual investors should understand the context of Warren’s words when he stated bonds were “a really dumb” investment compared to stocks. Undoubtedly, he teaches us much about identifying attractive equity market business models- but remember that his investment objectives, risk tolerance, and investment time horizon are likely different than the average investor.

The composition of assets within a portfolio is primarily driven by the investor’s objectives. Objectives are primarily designed around achieving or maintaining a particular lifestyle. This may be a specific figure of net worth, income, gifting, or philanthropic activity. Mr. Buffett is driven by a very different purpose. His objective is driven by stockholders, who require continual quarter-over-quarter, year-over-year growth…in perpetuity. In a sense, Warren the man is really Warren the corporation and since a corporation’s lifespan is essentially endless, he will necessarily have different objectives than the ordinary investor. For most investors, income or net worth goals can be finite and established in order to get across the peace-of-mind finish line. Total return in perpetuity is not the sole driver of objectives for your average individual. Instead, locking in a fixed income and higher bond allocation is often necessary to achieve the peace of mind at a particular stage of life.

Objectives and time horizon drive portfolio risk, and risk drives security selection. Mr. Buffett needs to build a portfolio of assets that are likely to provide high levels of cash-flow far into the future and that can offset catastrophe insurance losses, which typically occur irregularly. On the other hand, our average investor holds a portion of their wealth in fixed income for two different life scenarios. Firstly, when they want to shelter a portion of the wealth they have accumulated throughout life. The second scenario is for investors who want serenity and optionality regarding their investment portfolios up to that point of ultimate wealth accumulation. This is in case of a job loss, large health expense, or even to take advantage of a stock market swoon during times of elevated valuations. Perhaps, the latter is why Mr. Buffett’s portfolio is currently 37% invested in cash and bonds, providing a bit of an incongruity to his “dumb” investment comment. That said, he has an added benefit of earning cash-flows from his various wholly-owned, underlying businesses to cover large one-off expenses. As for an individual investor, the potential of incurring an emergency or large one-time expense will drive an allocation to fixed rate, creditworthy bond assets.

To understand where Mr. Buffett falls on the risk-tolerance spectrum, look no further than the concentration of his stock ownership- both as a percent of his overall investment portfolio and in individual holdings.[1] This demonstrates Mr. Buffett is willing to stomach a much higher hit to principal than that of his competitors and even your average hedge fund manager. Of his insurance company counterparts, my calculations show Progressive Corporation having the next highest allocation to stocks at only 12% vs. 63% for Berkshire.[2] The fact he has been so successful designing a portfolio in such a way for so long is the essence of his genius. That said, this level of risk tolerance is unique and relatively very high.

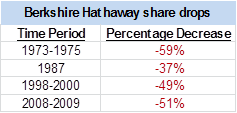

Shareholder returns are directly connected to this portfolio risk and have experienced significant volatility in times of stress.

Source: Berkshire Hathaway 2017 Annual Report

Though long-term holders have obviously been rewarded, these types of stock swoons may be unpalatable for investors with a low tolerance for volatility. Also, most investors do not carry a perpetual investment horizon like that of Berkshire Hathaway, which will continue long after Warren Buffett and should invest as such. Assuming continued, long-term, economic growth and proper security selection, the company has time on its side to recover from economic calamities and short term volatility. Individual investors do not always have this benefit. Take for instance 1999-2009, which was a lost decade of stock returns – unlike for bonds.

To sum it up, Mr. Buffett’s anti-bond attitude must be understood in the context of his unique investment objectives, high tolerance for risk, and his perpetual holding period. He said it best while being interview on Monday morning by CNBC: “You will not be way happier if you double your net worth.” Is trying to achieve this with unnecessary or concentrated risk in any market worth sacrificing your peace of mind and long term goals?

[1] Buffett’s top 15 holdings of his publicly traded portfolio are 85.75% of the overall portfolio. Wells Fargo is the largest holding, followed by Apple at 17.16% and 16.47%, respectively.

[2] Source: Bloomberg